Pioneer Credit Strategic Outlook

Sidney: Hi, guys. Welcome to CRIISP TV. I'm joined today by Keith John, the managing director of Pioneer Credit. Thank you for joining us, Keith.

Keith: Thank you, Sidney.

Sidney: Excellent. Just a brief introduction to Pioneer Credit. Pioneer Credit is now providing, I think nearly 200,000 customers Australia-wide, with the services that are aimed at helping them achieve both their financial goals, using their process to help clients reduce their debt and alleviate financial distress. So we'll be providing everybody with a brief overview of Pioneer Credit, following their viewing of this Q&A in the sections of this email. But, Keith, just for the audience who aren't aware yet, can you provide us with a bit of history of Pioneer Credit to date? I mean, 200,000 clients Australia-wide, is obviously an amazing achievement and you guys obviously have a process that's working well. So do you mind diving a bit deeper into that, just to start with?

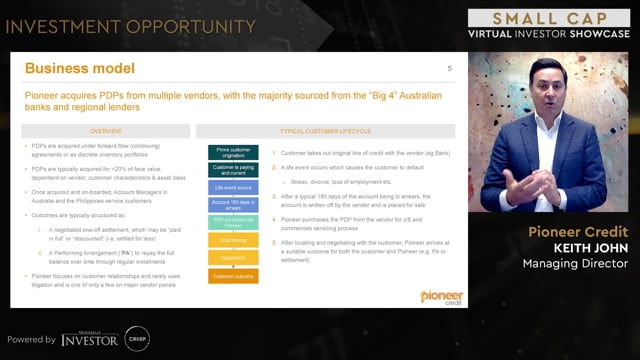

Keith: Yeah, for sure. Appreciate the opportunity, thank you. So look, Pioneer is a financial services provider. We operate under an Australian credit license and what we do is, we buy non-performing loans predominantly off the major banks. So credit cards and personal loans that are generally about 180 days past due. And these are customers that have generally had some sort of life event, lost their job, divorce, sickness, maybe domestic violence. And what's happened is, they've then defaulted on their credit. And we work with those customers over time to help them get back on track. So we manage all of these customers. We contact them, we service them by providing time and also ways to work out the debt that they might currently own, and give them the ability to pay that off over time. Like you said, we've got about 200,000 customers across Australia. We've invested about half a billion dollars Australian over the course of the last five or six years in particular, into buying these portfolios and working with these customers over time, so that we can get them back on track and obviously also for the benefit of our shareholders.

Sidney: Okay. So it's obviously a very sensitive client interaction, as you mentioned, a lot of them have experienced a life event. So in terms of the way you differentiate yourself from other purchasers of debt, is there a particular process that Pioneer Credit takes in engaging with clients?

Keith: Yeah, absolutely, Sidney. So the first thing is, we are one of the only people in Australia, or groups in Australia, that only buys debt and doesn't do work for third parties. And that's an important differentiation because we are not a debt collector. Okay? We don't have a debt collection license. We service customers and help them get through a range of situations. The way that we do that, is quite honestly, by being very human, having a human conversation and trying to understand what it is that we need to solve or help solve for that consumer, so that they can get back on track. Invariably, with lots of people, the challenges that they experience are temporary, short term, and they just need time. Australians are generally very positive people. They've got a huge desire to get ahead and we help facilitate that through the processes that we have, and through our call center, and customer service team that are there for our customers.

Sidney: Okay, great. And I think attributed to you guys is some recognition around your growth. What do you think is behind that growth to date? I mean, to get to where you are now, you've got your addressable market and you've tapped into that successfully. Tell us about the team behind Pioneer Credit and how that's gotten you to where you are today.

Keith: Yeah, thank you. So I founded Pioneer Credit probably 20-odd years ago now. We listed on the ASX six or seven years ago. And during that time in particular, we've been growing relatively quickly as we scale up our operation and as the sale of debt becomes more prominent in Australia. We've got a team that's been with us for a long period of time and is very stable, that work towards helping these customers. But the main reason for our growth, in addition to our team and the way that we service the customers, is the belief that the banks have in us that we will treat those customers well. We will protect their brand well, as well as our brand, by delivering the right outcome to the consumers. So when the banks are looking to sell portfolios of customers that are experiencing either some form of hardship or financial distress, they want to sell it to a group that's a very safe pair of hands, and that's Pioneer. That's exactly what we represent to the banks and it's why they feel comfortable in handing their most vulnerable customers over to us.

Sidney: And you've maintained those relationships with the banks, I assume. And there's a lot of effort that goes into that. And you see that as something that's going to drive this growth in the near and long term as well, I assume.

Keith: Yeah. Absolutely. I mean, out of the back of the Hayne Royal Commission, what we saw was an increase in expectation of consumers about how they should be treated and how they should be regarded by financial services providers. And that certainly flows down to us and is something that we've been very, very clear about from the beginning. Our consumers, our customers, are our number one priority and our customers are not the banks. That's our customer acquisition program, for lack of a better description. And we've got very strong obligations to the banks and to looking after their brands, but we cannot and we will not be successful unless our customers are the number one priority. And unless they receive a great level of service and that's what we strive to do every day, like all good organization.

Sidney: Yeah. Maybe we can dive deeper into that. Obviously a lot of, like you said, organizations obviously aim to put the customer first, but you've made it the main subject of this interview, which obviously shows the importance you attribute to that. Give me some examples of customers that you've sort of understood, or heard, or firsthand experiences, in relation to your product at Pioneer Credit. I think it'd be great for the audience to hear about that.

Keith: Yeah. Well, I think the first thing that people need to understand, Sidney, is financial distress doesn't just affect people from lower socioeconomic environments. It actually affects everyone across the broad spectrum of Australian society. And we genuinely have a portfolio that represents Australian society. So we've got everyone from lawyers and doctors, through to casual workers that might be working in a supermarket, who are customers of ours. And generally speaking, what occurs is, they have a lack of financial education or like most Australians, they're simply living to the edge of their means, but then this event comes through and we work with them over time. Sometimes that's as simple as saying, "Look, we understand that you'll be back on track in four weeks, or six weeks, or eight weeks. And let's work through that together and let's keep in touch, and we can work out an arrangement at the end of that."

Other times we've got customers that might have an illness, for example, and whilst we don't want to make life more difficult for that customer and certainly that's not what we do, but we want to understand, "How long will it take you to recover from this?" And then give them the space to go and do that, and then we can sort out their situation. So the first point of dealing with any of our customers is to relieve the stress that comes with having an obligation which you can't meet. From there, it really is about having a human conversation with that customer and addressing their needs. And the way we do that, quite unlike most contact centers, is we do not have call scripts in this business. So the way that you would receive service, Sidney, in your particular case from one of our people, might be entirely different to the way that I receive service, but it'll always be delivered with honesty, with integrity, and with your care at the forefront of our thought.

Sidney: Excellent. I think that's an excellent summary on what is differentiating your business from the rest of the market. So you're in obviously a growing sector and you've managed to master the client engagement process there, and you've outlined the importance of that. And you've also outlined the importance of the maintenance of the relationships with the banks. They're happy to have you in partnership. Now, for prospective shareholders out there of which this Q&A will ideally be going out to, what is the strategic outlook for Pioneer Credit and what are some milestones that should excite them in the near term?

Keith: Yeah, I mean, look, Pioneer's had a challenging couple of years, following a scheme of arrangement that was entered into in 2019, that was terminated last year at the height of COVID. And after that, we needed to refinance. We refinanced at that stage, paying what is a very high interest rate, but did so in a manner that protected our shareholders. So we didn't do a dilutive equity issue at the time. We are now about to commence refinancing again, to reduce our cost of funds and really leverage the profitability that sits within this business. So number one is to complete our refinance and to get that complete. And we expect that we should be in a position to have that done in the next few months. That's the first thing. The second is, we're in a fantastic market at the moment. Where we are currently is, Pioneer's the second largest purchaser of debt in the market.

And really a lot of our competition has changed and moved to the sidelines. Banks want very, very, very safe hands dealing with customers, particularly out the back of COVID and the challenges that the pandemic has brought to Australian consumers. Pioneer is one of the very few groups that are trusted to do that. And we expect over the next couple of years that we are going to have many, many purchasing opportunities, that will see us not only return to the levels of investment that we made in portfolios going back only two years ago, of about $80 million, but beyond that, to a $100, $120, to $150 million over the next couple of years. So we see a big opportunity for growth, both in the investment in these consumers, and then obviously bringing through those consumers into our business and working with them over time, to return them to financial health and obviously for the benefit of our shareholders as well.

Sidney: Excellent. Well, Keith, I think you've given us an extremely extensive rundown of the position you guys are in, the position you guys were in, and where you are looking to go in the next 10 to 12 months, which is excellent. And I think it's given us a rudimentary understanding of Pioneer Credit and your ambition. I want to thank you for joining us today. And, Keith, what we'll be doing is, at the bottom of this video, there'll be a link to contact a representative from Pioneer Credit, to discuss the opportunity in more detail. And, Keith, is there anything else you want to add before we part ways today?

Keith: Look, no, just to thank you and your investors for their time. There is a lot of information about Pioneer. We publish a lot to the ASX. We welcome any queries and hopefully we'll welcome you on board as a shareholder soon.

Sidney: Excellent. Thank you for your time, Keith.

Keith: Thank you, Sidney.

More articles

- 20 July 2022

Interview with ausbiz

Managing Director, Keith John, speaks with ausbiz about FY21 EBITDA guidance and future growth of Purchased Debt Portfolios. Watch now or read the transcript below.

Read more about Interview with ausbiz - 19 July 2022

Small Cap Virtual Investor Showcase Presentation

Pioneer Credit Managing Director Keith John presents to the Wholesale Investor May 2021 Small Cap Virtual Investor Showcase. Watch the video or read the transcript below.

Read more about Small Cap Virtual Investor Showcase Presentation

Get in touch

If you have any questions, or would like more information, our team is here to help.

Investor Centre